By Alexandra Norris and Leora Klapper

Working on a farm, whether growing crops or raising animals, is hard work. The days are long, and the risk of drought, flood, or damaging storm is always in the background.

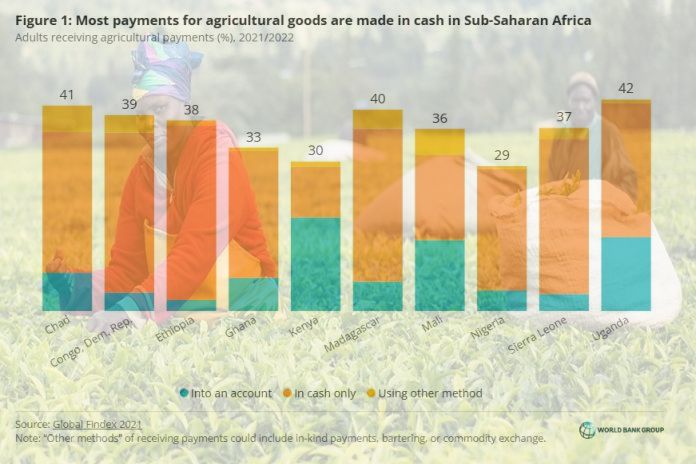

Despite how hard it is, one in three adults in Sub-Saharan Africa receive agricultural payments, making them an important source of household income, according to the latest Global Findex 2021 regional note, Digitalizing Agricultural Payments in Sub-Saharan Africa. In economies like Chad, Madagascar, and Democratic Republic of Congo, 40 percent or more of the population earns money through agriculture.

Receiving those payments digitally is more convenient and safer than cash for agricultural workers. Cash payments are vulnerable to theft and often require recipients to travel to a central collection point – neither easy nor convenient if you already work long, physical days.

Yet, more than 140 million agricultural payment recipients in Sub-Saharan Africa, including 66 million women, are paid only in cash. Making some or all these payments through digital channels presents a significant, untapped opportunity to expand financial inclusion for Africa’s agricultural producers.

Digitalizing payments through global agricultural supply chains

While many farmers in Sub-Saharan Africa sell through relatively informal, local markets, an estimated 20 percent participate in formal value chains involving governments or private buyers. These agricultural producers have the most immediate opportunities to receive payments digitally, given that the broader trade ecosystem in which they participate is digitalized.

There is already some precedent for successfully digitalizing payments connected to larger and more digital wholesale supply chains. For example, in Kenya, some wholesale buyers have invested in digitizing payments to their farmers, reporting that the benefits and cost savings outweigh the start-up costs. These actions on the part of payers, combined with Kenya’s relatively high account ownership rate – 80 percent among agricultural payment recipients – has helped drive agricultural payment digitalization in the country. As of 2021, around 63 percent of Kenya’s agricultural producers were being paid into an account.

Barriers to agricultural payment digitalization span recipients and payers

While the opportunities and benefits of digitalizing agricultural payments are significant, there are barriers that make it difficult to expand digital financial service usage for agricultural sellers. Not all those barriers relate to foundational access to finance. For example, nearly 60 percent of adults receiving agricultural payments only in cash in Sub-Saharan Africa have a mobile phone and around 40 percent of them have a bank account. These banked agricultural producers may sell to buyers who refuse to make payments into an account, or they may live in a place with few accessible cash out locations or merchants who accept digital payments.

Focused advocacy and technical assistance may be necessary to help both recipients and buyers/payers adopt digital payments, as has been done in Ghana’s coca supply chain. Additionally, individuals selling agricultural products directly to consumers can benefit from improved “fast payment” systems that link banks through a digital infrastructure.

To see more Global Findex 2021 data on agricultural payments in Sub-Saharan Africa, download our latest regional note.