Overview of Argentina’s economic situation under president Javier Gerardo Milei

Since taking office in December 2023, Javier Milei has embarked on shock therapy to reshape Argentina’s economy. Milei inherited an unenviable situation, with inflation over 100 percent, a gaping fiscal deficit and GDP already declining before he took office. Below is a look at how Argentina’s economy has fared under Milei during his first year in charge.

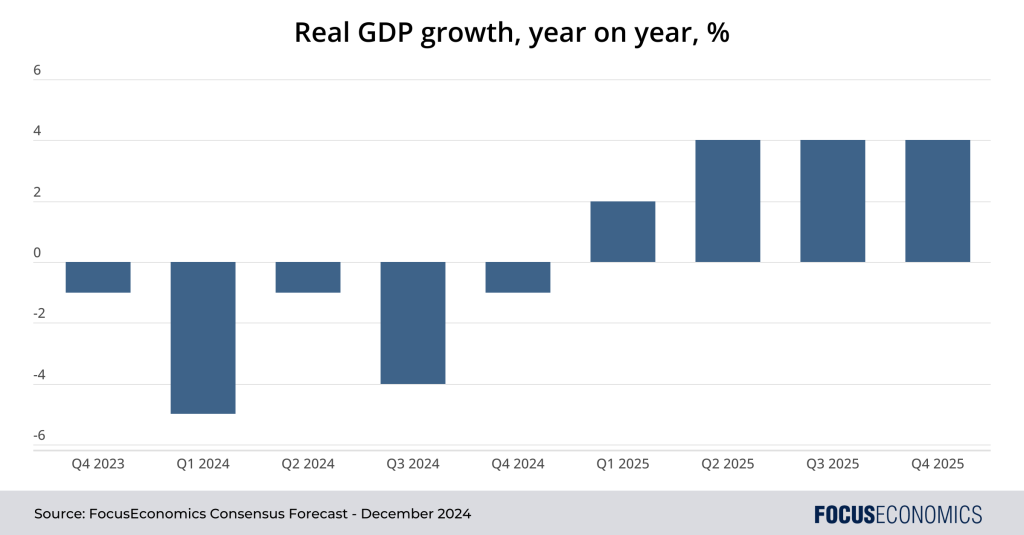

GDP growth

Argentinian GDP likely shrank year on year for the sixth consecutive quarter in Q3 2024 due to harsh government spending cuts. However, the economy should have rebounded in quarter-on-quarter terms following three straight sequential contractions, thus emerging from recession, thanks to improving real wages, stronger credit provision, and the positive impact of the liberalizing reforms approved since Milei took office.

Inflation

Year-on-year inflation declined for the sixth straight month in October. Also in October, month-on-month inflation fell to 2.7 percent, a far cry from the peak of 25.5 percent reached in December 2023. Lower inflation has gone hand in hand with a recovery in real wages, boding well for consumer spending.

Fiscal balance

The government has run a fiscal surplus every month this year except July, a month which saw a deficit due to debt interest charges and bonus salary payments. This marks a sudden break from the deficits run under the previous administration – a deficit which grew particularly large in 2023 due to pre-election fiscal giveaways.

Interest rates

The central bank has cut its main policy rate by 98.0 percentage points since Milei took charge, though at 35.00 percent the rate is still among the world’s highest. Lower interest rates have helped boost credit to the economy; private-sector credit more than tripled in annual terms in September.

Exchange rates

Milei’s government has allowed the official currency to depreciate by around 2 percent per month against the US dollar following a one-off large currency devaluation last December. Given inflation has been above 2 percent under his term, the currency has thus strengthened in real terms, as fewer Argentinian products can be bought for the same amount of US dollars than before. Meanwhile, the gap between the official and main parallel rate had narrowed sharply to a little over 10 percent by late November. That said, resolving the byzantine web of different currency rates and restrictions is still an outstanding task for the administration.

Key economic policies implemented by Milei

Despite Milei’s La Libertad Avanza party having very little parliamentary representation, the president has managed to approve a number of reforms during his first year in office, mainly through two key bills: The “Ley Bases”, and an earlier “Decree of Necessity and Urgency”. Below is an overview of approved measures:

Deregulation and market liberalization

The authorities have relaxed tenancy laws in order to boost the supply of rental properties, and tweaked employment rules in favor of employers in order to make the labor market less rigid. Moreover, the authorities have set the stage for several state-owned firms to be privatized, including the national flag carrier, Aerolineas Argentinas.

Tax reforms and fiscal policy changes

The government has implemented a new regime to incentivize investment (RIGI). It includes tax and legal concessions to firms making large investments in strategic economic sectors such as energy, raw materials and technology. Moreover, the government has eliminated a key import tax, pared back public spending dramatically, and announced a tax amnesty that had reportedly raised USD 18 billion by late October.

Monetary policy adjustments

The central bank’s most notable policy change, in addition to slashing its key interest rate by 98.0 percentage points, has been to abruptly end monetary financing of the fiscal deficit, which was a commonplace practice under the previous administration. This has helped to reduce the money supply and inflation in turn.

Impact of Milei’s policies on poverty and inequality

Though Milei’s policies have been successful in some senses – they have helped to rein in inflation and boost credit for instance – there has also been a darker side. The poverty rate has risen to 53 percent from 42 percent in H2 2023, and inequality has spiked, with wages for salaried employees rising far faster than those in the informal sector year to date. Thus far, the president’s approval rating has held up well despite these challenges, but that might not last if economic conditions don’t improve substantially soon.

Support from global financial institutions

Argentina has a financial program in place with the International Monetary Fund (IMF); the Fund has thus far disbursed over USD 40 billion under this arrangement, with over USD 5 billion dished out so far this year thanks to Milei’s commitment to fiscal discipline and structural reforms. The government is negotiating a new deal with the IMF, with fresh funding key to boosting central bank reserves and lifting capital controls (known locally as the “cepo”). The election of Donald Trump as US president is positive news in this regard: Trump’s political affinity with Milei could accelerate Argentina’s negotiations with the IMF and ultimately lead to a more generous support package than would have been the case under a Democrat administration.

Long-Term prospects for Argentina’s economy

After contracting for the second straight year in 2024, our Consensus is for the economy to bounce back in 2025 and record growth well above the Latin American average. Panelists have become increasingly optimistic about the outlook in recent months in light of strong reform progress and lower-than-expected inflation; our Consensus for 2025 GDP growth has been raised by 0.5 percentage points since the middle of this year.

Both the industrial and services sectors should rebound in 2025 as Argentina’s inflation continues to decline, credit remains robust, and the business environment improves. That said, agricultural growth will slow following a bumper 2024 harvest on the back of improved weather conditions. Moreover, investment will be capped going forward by the lack of clarity regarding the lifting of capital controls and the shape of the future currency regime. Capital controls are likely to remain in place until after the 2025 midterm elections, as Milei looks to avoid provoking any sort of economic instability that could harm his party’s chances.

Beyond 2025, Argentina’s rate of economic expansion should ease but remain above the regional average. The country holds immense economic promise: It has among the world’s largest lithium and gas reserves, and huge renewable energy potential. If it continues along the path of fiscal sobriety and economic liberalization laid out by the current administration, living standards could improve substantially going forward. That said, risks abound. Chief among them is the prospect of a messy end to the current managed exchange rate regime leading to a collapse in the currency.

Then there is an intensification of opposition from political and social groups; this will grow more likely if the economy doesn’t pick up and could test the sustainability of Milei’s economic reforms. Extreme weather is also an issue: Agricultural output collapsed by 24 percent in 2023 due to drought for instance. And, finally, a return to fiscal profligacy and inflation is on the cards if the Peronist movement wins the 2027 general elections. In short, at this stage, it would still take a brave investor to go all in on Argentina’s economic future.

Insight from our analysts

EIU analysts commented on fiscal policy:

“In a bid to keep spending under control, the government announced a new fiscal rule in its 2025 budget; the rule says that the primary fiscal surplus must equal debt payments in order to reach overall fiscal balance. If fiscal balance is at risk, the government will cut discretionary spending. In line with the Milei administration’s libertarian views, the government says that it will not use fiscal policy as a counter-cyclical tool. We expect the government to maintain an overall fiscal balance in 2025, owing to spending constraint, but also reflecting increased revenue collection amid a firm economic recovery. We expect austere fiscal policy and nominal GDP growth to bring down the public debt/GDP ratio from 80.4 percent of GDP in 2024 to 62.9 percent of GDP in 2029.”

On inflation, Itaú Unibanco analysts, said:

“We expect lower inflation in 2024 and 2025. We now foresee a 2024 inflation rate of 120 percent at year-end, down from 125 percent in our previous scenario. For 2025 we see inflation at 35 percent, down from 45 percent in our previous scenario. In our view, the government’s strategy of obtaining dollar financing to cover debt maturities in 2025 will allow it to maintain the crawling peg policy next year with the objective of speeding up the disinflation process. Also, lower country risk may lead the government to return to international markets next year.”

On the exchange rate, Goldman Sachs’ Sergio Armella, said:

“President Milei stated that if inflation remains stable for two more months, the exchange rate depreciation crawl will be lowered to 1 percent from the 2 percent that has been maintained since January. In our view, the recent interest rate cut to 35 percent by the central bank coupled with a deceleration of the FX crawl suggest that capital controls are likely to remain in place for a while longer. In our assessment, the currency has moved towards an overvaluation and tighter monetary policy and a more flexible exchange rate regime will be needed down the road to anchor the economy.”

delivers insights for action")