By Adamon Mukasa and Anthony Simpasa

The implementation of the United Nations’ Agenda 2030 for sustainable development (https://apo-opa.co/4g2kWSb) and the African Union’s Agenda 2063 (https://apo-opa.co/4767Ak0) hinges on Africa’s ability to mobilize sufficient and timely financial resources. The recently released African Economic Outlook (AEO) 2024 (https://apo-opa.co/3yWpFEs) report by the African Development Bank estimates that the continent needs to close, by 2030, an annual financing gap of US$402.2 billion to fast-track its structural transformation process. Scaling up domestic resource mobilization (DRM) will be key to achieving that objective.

African governments have always recognised the central role of increased mobilization and effective use of domestic resources to achieving sustainable development goals (SDGs) and other national development objectives. Through the 2015 Addis Ababa Action Agenda (https://apo-opa.co/4cG67ly), African leaders reaffirmed their commitment to “further strengthening the mobilization and effective use of domestic resources”, underscored by the principle of national ownership established in the Paris Declaration on Aid Effectiveness (https://apo-opa.co/3WZXZ9v). African governments have thus stepped up their policy levers towards improvement of DRM and combatting tax evasion and avoidance. These initiatives include, for example, the work of the African Union Development Agency-New Partnership for Africa’s Development (AUDA-NEPAD) (https://apo-opa.co/3ARAhEU), the High-Level Panel on Illicit Financial Flows (IFFs) (https://apo-opa.co/4cK2efo), the African Union Assembly Special Declaration on IFFs (https://apo-opa.co/4g1ixXN), the Africa Initiative of the Global Forum on Transparency and Exchange of Information for tax purposes (https://apo-opa.co/4gfrvRJ), the African Tax Administration Forum (https://apo-opa.co/4dWXpA9), and the establishment of Medium-Term Revenue Strategies (MTRS) (https://apo-opa.co/3MjW4HY). These initiatives emphasize the need for mobilization of domestic resources at scale and addressing resource leakages.

Stocktaking of Africa’s DRM progress

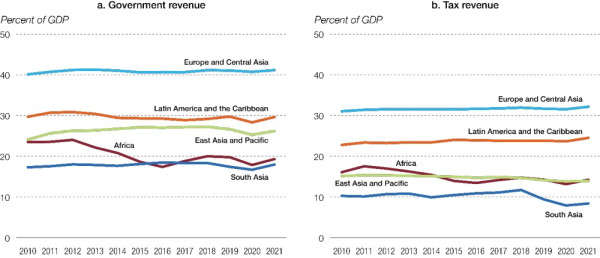

Africa has increasingly mobilized its domestic resources to finance its development priorities in sectors such as health and education, infrastructure development, industrialization, and agriculture. In absolute terms, Africa’s government revenues (tax and non-tax revenues, excluding grants) increased by almost 40 percent from about US$435 billion in 2015 to US$604 billion in 2022 and are projected to reach about US$626 billion in 2025. Tax revenues account for more than 75 percent of the continent’s total domestically generated revenues. However, in relative terms, the continent underperforms its peers. Data from the AEO 2024 indicate that Africa’s average general government revenue declined substantially from 23.5 percent of GDP in 2010 to 19.3 percent of GDP in 2021. This is due to a steady decline in tax revenues, over the same period, from 16.1 percent of GDP in 2010 to 14.2 percent of GDP in 2021. In particular, since 2015, Africa’s average tax revenue ratio relative to GDP has consistently been below the 15 percent minimum (https://apo-opa.co/3X4DYPi) required for a developing country to adequately finance its SDGs. Africa’s revenue ratio is well below the average for Latin America (23.9 percent) and less than half the average for Europe and Central Asia (31.7 percent). Africa’s average low tax revenue ratio mask significant heterogeneity among individual African countries. As shown in figure 2, the average tax-to-GDP ratio over 2015-2025 falls short of the 15 percent threshold in 34 countries, spread across all of Africa’s five regions, calling therefore for urgent actions to scale up DRM and align it with financing needs for structural transformation.

Aligning DRM with financing needs for structural transformation

According to findings in the AEO (2024), African countries need to increase their tax-to-GDP ratio by a median value of about 13.2 percentage points—bringing the current median ratio to 27.2 percent of GDP—to be able to close the estimated financing gap for structural transformation. This is under the assumption that additional mobilized tax revenues are efficiently deployed and allocated to financing structural transformation. While the estimated tax effort may be within reach of many African countries, it remains unattainable for others given their relative low potential tax-to-GDP ratio. Hence, out of the 39 African countries with data on tax capacity, the report found that in 18 countries (46.2 percent of them), the level of tax-to-GDP ratio required to mobilize resources for structural transformation exceeds the maximum amount of tax revenues that could be collected given socioeconomic and institutional factors (Figure 3). This means that even if those countries exhaust their current tax capacity, they may not be able to close their respective estimated financing gap by 2030.

Scaling up resources to fast-track structural transformation in Africa will require addressing underlying challenges and constraints to domestic resource mobilization. These challenges include inter alia: i) High levels of informality (about 86 percent of total jobs on the continent are informal) (https://apo-opa.co/3T4YKwQ); ii) Weak tax administration capacities (https://apo-opa.co/4cKmfm3), leading to inefficient tax collection; iii) Complex tax law and rules, which reduce compliance rates; iv) Low domestic savings (prior to the pandemic, Africa had one of the lowest gross domestic savings rates in the world, at 13.6 percent of GDP)1; v) Endemic corruption (https://apo-opa.co/4g2luaH) (Africa loses annually in IFFs about US$89 billion) (https://apo-opa.co/3MmfvzX); and vi) Inefficient and expensive tax collection systems.

On the last point in particular, data suggest that between 2000 and 2021 African countries collected only 24 percent of the VAT revenues annually – the lowest rate in the world – that they could otherwise have collected with full compliance and without tax exemptions. The AEO (2024) report has therefore estimated that by just increasing the VAT efficiency ratio to the level currently achieved by high-performing developing countries in other regions—those with a VAT efficiency rate of at least 70 percent—African countries could raise their current median VAT revenues (as a share of GDP) by as much as 7.9 percentage points, equivalent to a median value of about US$1.9 billion. In aggregate terms, improving VAT efficiency ratio could translate into additional VAT revenues of US$171 billion (or 42.5 percent of Africa’s US$402.2 billion financing gap).

There is a long way to go to make DRM work for Africa’s structural transformation. To move fast, policy priority should be given to improving the transparency of the tax system, widen the tax base, enhance enforcement, mitigate compliance risks, and ultimately stimulate voluntary compliance by strengthening the social contract via enhanced provision of public goods and services to address widespread implicit taxation and increase compliance; increasing non-tax revenues such as property income, royalties, fines, penalties, forfeits, and business permits; enhance the formalization of the informal economy and, digitalization of tax collection systems to curb corruption, thereby enhance revenue collection.

Distributed by APO Group on behalf of African Development Bank Group (AfDB).